These days, many people talk about the economics of traffic. Japanese experts estimate that traffic is robbing people of P2-3 billion every day. All the time lost translates to work that can’t be done, kids who never see their parents, and more. Countless life-changing opportunities are lost waiting on EDSA, C5 or whatever congested patch of road you traverse on a daily basis.

Many people in the Philippines respond to traffic by buying cars. People choose to buy cars for selfish—yet also completely understandable—reasons. A car allows you to travel in comfort, safety and convenience, at the expense of congesting roads for others. But even if driving a car adds to the traffic slowing down everyone else, it’s hard to ask people to not look out for themselves and their loved ones first.

It just makes economic sense. But does it, really? Let’s break it down here.

To own a car, you first have to come up with the money to buy it (obviously). If you have the money to pay cash for a car, then awesome! But for most people, they’ll have to go to a bank to get financing. The purchase price of a car is split into a down payment and a bundle of amortization payments, which are usually paid monthly over the term of the car loan. The larger a down payment you are able to come up with, the lower your monthly payment.

Next come the immediate running costs of owning a car. The most obvious one is fuel—you have to fill your car up for it to be of any use. Fuel costs will depend on the car you have and how often you use it. You’ve also got to pay for parking your car. Fortunate people will have free parking both at home and at work or school, but most people will have to pay for one or the other (or both).

Finally, there are the other non-immediate running costs of car ownership: maintenance, registration and insurance. These are costs that people don’t always associate with car ownership because they aren’t paid as often, but they certainly have to factor into one’s calculation.

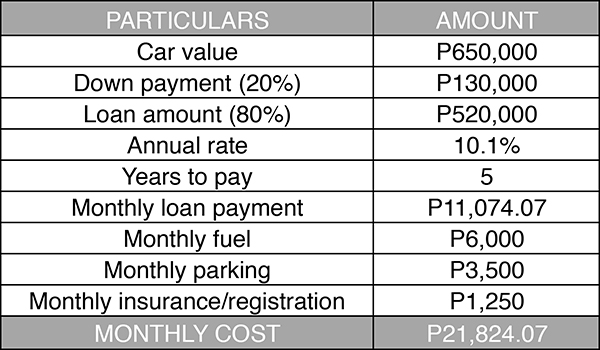

How much do all these costs add up to? I went through this exercise recently because I considered buying a car myself. Looking at a middle-of-the-road small car—say, a Toyota Wigo or a Mitsubishi Mirage—I asked some friends about their costs, and did a spreadsheet calculation to estimate my own. Here, the saying “Your Mileage May Vary” is very appropriate. My estimated cost of buying and owning a brand-new car is shown below:

A sample monthly cost of ownership

So even if you could make a P130,000 down payment—the lowest most banks will take—you’re still looking at a monthly amortization payment of over P11,000 over five years. And at over P20,000 a month in total costs—more than what many jobs pay in the Philippines—car ownership is a huge financial burden, making even the people who can afford cars feel poor.

Altogether, P21,824.07 sounds like quite a bit, but that’s just the private cost of car ownership. The public costs—congestion, pollution, accident risks and the often-subsidized portion of parking—are charged to everyone else on the road and in our city. If car owners had to face these costs—which is the principle behind policies such as Singapore’s road pricing—their costs would go up even more, and surely fewer people would choose driving.

At over P20,000 a month in total costs—more than what many jobs pay in the Philippines—car ownership is a huge financial burden

What are the alternatives to owning a car? Here are a few alternatives that people should consider, with typical costs listed as well:

1. Use the public transport system. And I mean any combination of MRT, bus, taxi and TNVS. Let’s go for a high-end estimate and assume someone does not take trains, buses or jeeps, and instead takes a P300 TNVS trip, two ways each day, for 20 workdays a month. That’s P12,000 a month to commute to and from work, give or take.

2. Buy a motorcycle. Motorbikes and scooters these days can be had for anywhere from P40,000 to P150,000, with much higher prices at the top end. For many, these will give the same mobility and freedom as a car. They take up less space on the road, but they do still cost society in the form of pollution and accident risks.

3. Buy a decent bicycle. There’s a wide range of bicycles on the market, but let’s go with Andy Leuterio’s recommendations and skip the budget bikes. After buying a bike and accessories such as lights, a lock, a pump and a helmet, perhaps you’ll end up spending around P22,000 to P50,000 for a decent bike-commuting kit, with much higher prices for top-end bicycles.

4. Buy an electric scooter or e-bike. These new Personal Mobility Devices represent a halfway compromise between bicycles and motorcycles. Electric scooters have a price range from P18,000 at the low end to over P200,000 for high-end models that can match the range and speed of motorcycles. While these vehicles have no tailpipe emissions, they still present safety risks in the hands of inexperienced drivers.

5. Rent a dwelling place near your work. For people who are already renting, the money that would have gone into monthly car payments may let you live close enough to walk to where you work.

What did I end up doing? I ended up buying a bicycle. And another bicycle. And an electric scooter. All for less than the cost of the down payment for my hypothetical car. Using those—plus the occasional TNVS trip—has been quite the adventure for me, and one which I recommend to people trying to free themselves from traffic congestion.

Comments